Chapter 1: The Poker Chip Fallacy

Technology has a bad habit of solving the wrong problem perfectly.

In my earlier article, “The Death of the Wallet,” we explored how the industry is wasting millions trying to digitize a leather pocket. We are building passive containers for a world that requires active agents. But if the “Wallet” is the wrong container, what about the thing we are trying to put inside it?

For the last decade, the smartest minds in fintech and crypto have been obsessed with Tokenization. The pitch is intoxicatingly simple: we took music and turned it into MP3s. We took photos and turned them into JPEGs. Now, we will take financial assets—stocks, bonds, real estate, invoices—and turn them into Tokens.

We view this as inevitable. We assume that if we can just wrap a complex asset in a cryptographic shell, it will become liquid, universal, legally compliant, and instantly transferable, flowing through the internet just like an email.

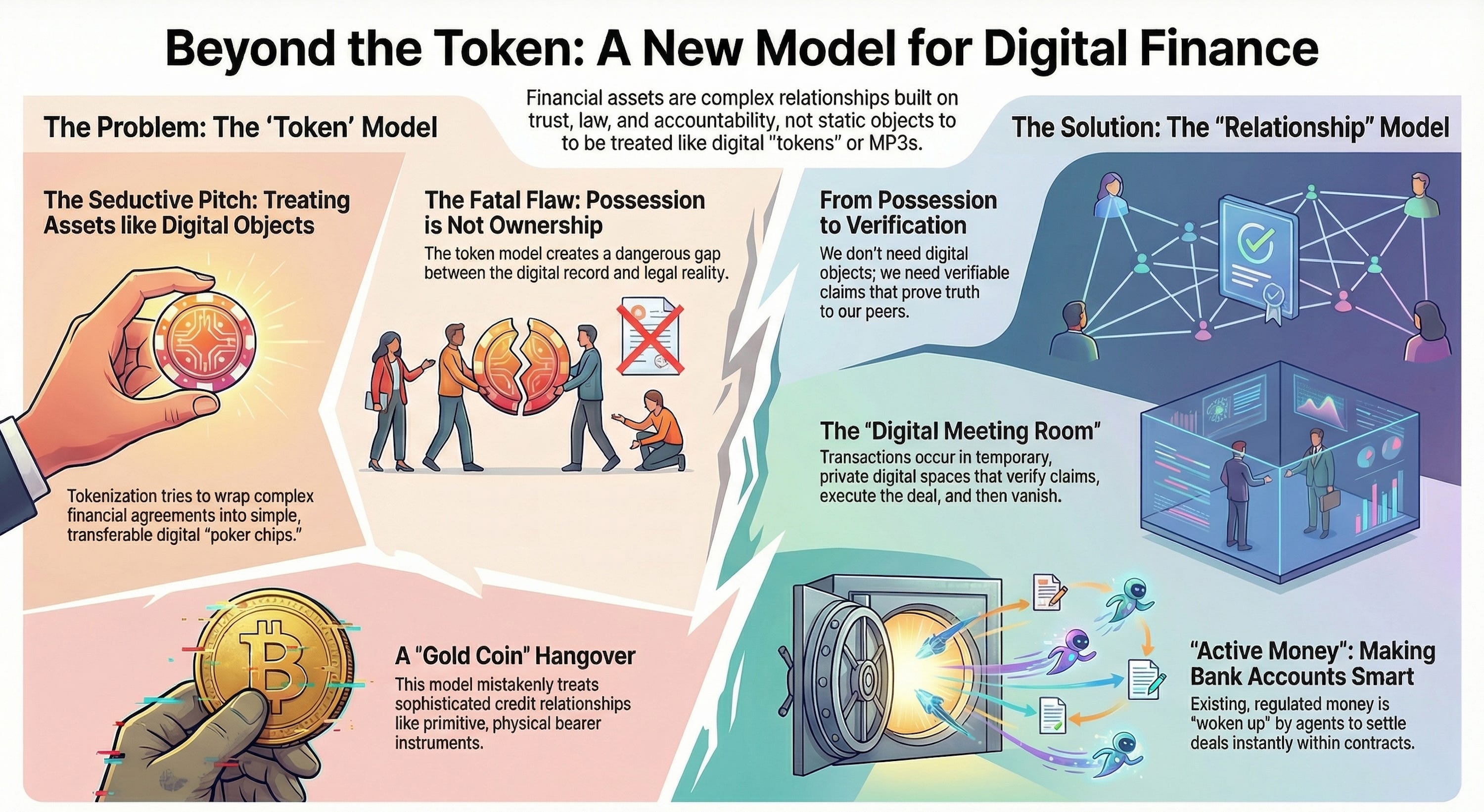

This is a seductive vision. It is also a fundamental category error.

By treating financial assets as “digital objects,” we are misinterpreting the very nature of finance. We are trying to force the complex, living web of human obligations and rights into the shape of a digital poker chip. And in doing so, we aren’t fixing the financial system; we are breaking the trust that holds it together.

The “Object” vs. The “Relationship”

To understand why tokenization is a trap, you have to understand the difference between a Static Asset and a Financial Obligation.

When we digitized music, it worked because a song is a static object. Once an MP3 is created, it stands alone. It doesn’t need to check back with the artist to see if they still feel like singing. It doesn’t depend on the legal jurisdiction of the listener. It is just data.

Finance is different. A loan is not a static object; it is a relationship over time. A stock share is not a digital marble you hold in your pocket; it is a bundle of legal rights and governance privileges recognized by a corporate entity. A mortgage is not a file; it is a complex, conditional agreement between a borrower, a lender, and the laws of the land.

Tokenization tries to flatten all this complexity into a “Bearer Instrument”—a digital object where possession equals ownership. The logic of the token is: “I hold the private key to this token, therefore I own the house.”

But in the real world, possession is not ownership. If a hacker steals the private key to your tokenized house, the legal system does not shrug and say, “Well, code is law, I guess it’s his house now.” The legal system intervenes. It reverts the ownership, if it can. In the world of unaccountable blockchains and bearer instruments, it’s not that simple.

This reveals the fatal flaw of the token model: it creates a dangerous gap between the Digital Record (what the blockchain says) and the Legal Reality (what the court says). The token claims to be the asset, but it is actually just a shadow. And when the shadow and the object disagree, the system collapses.

The “Gold Coin” Hangover

Why are we so obsessed with making finance look like digital objects? It is because our mental model of value is still stuck in the 17th century. We are suffering from a “Gold Coin” hangover.

For thousands of years, value was an object. If you held a gold coin, you held the value. If you dropped it in the ocean, the value was gone. It was simple, anonymous, and physical. Bitcoin brilliantly replicated this physics in the digital realm. It created a “digital gold coin” that relies on no one. If you lose your key, you lose your Bitcoin. The system works because Bitcoin has no off-chain reality; the map is the territory.

But traditional finance is not about gold coins, although liquid assets such as gold can back the financial system. It is about credit. It is about promises.

When you look at your bank balance, you aren’t looking at a pile of digital coins sitting in a vault. You are looking at a record of the bank’s promise to pay you. You don’t “hold” your money; the bank holds a liability to you.

Tokenization tries to drag us backward. It tries to turn these sophisticated relationships of credit and accountability back into dumb, digital bearer instruments. It asks us to treat a complex corporate bond like a gold coin.

This is why “Real World Asset” (RWA) tokenization projects keep failing or getting stuck in regulatory purgatory. They are trying to solve a trust problem with a data structure. They are trying to replace the need for an accountable issuer with a cryptographic lock.

The Alternative: Evidence, Not Objects

If the “Token” is the wrong metaphor, what is the right one?

If we shouldn’t be building digital poker chips, what should we be building?

The answer lies in moving from Possession to Verification. We don’t need digital objects that we carry around in wallets. We need Verifiable Claims that we present to peers.

Imagine the difference between a casino chip and a signed letter of credit.

The Chip (Token): Its value comes from possession. If I steal it, I can spend it. It is dumb and anonymous.

The Letter (Claim): Its value comes from the signature at the bottom. It says: “Bank A certifies that Timo is good for $10,000.”

The future of digital finance does not belong to the Chip. It belongs to the Letter. It always has.

We don’t need to “tokenize” a house to prove I own it. I just need a cryptographically signed credential from the land registry—a Verifiable Claim—that my Agent can present to a bank. I don’t need a “stablecoin” token to pay for coffee; I need a signed claim from my bank proving I have the funds, which my Agent transfers to the merchant.

This distinction changes everything. A Token asks you to trust the unaccountable network. A Verifiable Claim asks you to trust the accountable issuer. It restores the human and legal context to the transaction. It keeps the data private (no public ledger required) and the liability clear.

The industry is currently obsessed with manufacturing digital poker chips. But the real revolution isn’t in creating new objects to hold; it’s in creating new ways to prove what is true.

In the next chapter, we will explore where these claims actually are created and used—not in a wallet, but in the “Digital Meeting Room.”

Chapter 2: The Digital Meeting Room

If we accept that financial assets are not digital objects to be held, but relationships to be managed, a new problem immediately arises.

Where do these relationships live? Who or what manages their life cycle?

In the physical world, agreements happen in specific places. If we are signing a merger, we meet in a boardroom. If we are settling a diplomatic treaty, we meet in a secure embassy. If we are closing on a house, we meet at a notary’s office. (Except for in Finland, where we digitalized it.) If we buy groceries, we go to a grocery store that has a cashier. (Yes, buying groceries is an agreement between three parties. The buyer gets the carrots and the seller gets the money from the buyer’s bank.)

These rooms share a critical property: they are Contexts. They provide a secure environment where the conditions of the deal are obtained and verified. For example, identities are checked, documents are signed, and the deal is finalized. Crucially, once the deal is done, the people leave with the evidence about the completed deal, and the room goes dark. The room does not keep a permanent, public broadcast of every word that was spoken.

The digital world, as of today, has no equivalent to this room.

We have spent thirty years building an internet of “Pipes” (email, messaging, APIs) and “Platforms” (Amazon, Google, your Bank’s portal).

Pipes are insecure and securing them is laborious; you don’t sign a mortgage via email.

Platforms are secure, but they are feudal. To transact, you must enter their castle, follow their rules, and leave your data in their permanent database.

The crypto industry tried to solve this by building the “World Computer” (Ethereum). But they essentially built a meeting room with glass walls where every transaction is recorded forever, visible to everyone, and impossible to delete. They built a surveillance machine and called it privacy.

To fix finance, we need a third option. We need a digital infrastructure that functions like a secure, private, and disposable meeting room.

In the Internet Trust Layer, we call this the Context Agent.

The “Burner” Infrastructure

Think of a Context Agent as a “burner” server.

It is a piece of autonomous software spun up for the sole purpose of executing one specific deal. It is not a platform you log into. It is a temporary, neutral zone created by the participants.

Let’s go back to the house purchase.

In the Token Model, I send a “House Token” to your wallet, and you send a “Money Token” to mine. This happens on a public ledger. Everyone sees it. If the code has a bug, the money is gone and there’s typically nothing that the legal system can do to help you.

In the Relationship Model (ITL), our Person Agents spin up a Context Agent—a Digital Meeting Room.

Entry: My Agent enters the room and presents a Verifiable Claim: “I am Timo, and I have a valid credit from Bank A.”

Verification: Your Agent enters and presents a claim: “I am the Seller, and here is the digital title deed from the Land Registry.”

The Logic: The room contains a set of rigid, pre-agreed rules (a contract). It checks the proofs. Is the money real? Yes. Is the title clean? Yes.

The Swap: The room executes the swap. It issues a new claim to me (Title) and a new claim to you (Funds). Furthermore, all parties get a signed receipt, i.e. a cryptographically verifiable execution log of what happened.

The Vanishing: This is the most important part. Once the signed receipts are issued and there can be no further state changes in the transaction, the room deletes itself.

The infrastructure evaporates. The deal is done, the evidence delivered, and there’s no going back.

The Vanishing Ledger

This concept—the Ephemeral Context—is the antidote to the “Honeypot Problem” that plagues modern cybersecurity.

Today, every trade platform, every retailer, and every blockchain maintains a massive, permanent ledger of history. These databases are “honeypots”—treasure chests of data that hackers spend their lives trying to crack.

But why do we keep these records?

If I buy a coffee, does the coffee shop need to know my name and birthdate? Does the blockchain need to store that transaction for eternity on thousands of nodes across the world? No.

We only need the verifiable record for the participants to prove the deal happened.

In the ITL, that proof is moved from the Platform to the Participants.

When the Digital Meeting Room dissolves, the only record that remains is the cryptographic “receipt” (the signed transaction log) held in your private storage and my private storage. If there is a dispute later, either of us can show the receipt in court to prove what happened. But for the rest of the world, the transaction is invisible.

This creates a digital economy that is as private as cash but as accountable as a wire transfer.

Deterministic Trust

The magic of this “Meeting Room” is that it removes the need for a permanent middleman to “settle” the trade.

In traditional finance, we wait T+2 days for trades to settle because we are waiting for humans and back-office servers to reconcile different ledgers. We are waiting for them to agree that what happened actually happened.

The Context Agent is Deterministic. It is a machine that follows a strict flow chart whose logic is publicly advertised. It cannot be bribed. It cannot get tired. It cannot “forget” to file the paperwork. It cannot be in an unknown state. If the inputs (the Verifiable Claims) are valid, the output (the Settlement) is instant and guaranteed.

We don’t need a “Token” to travel across a network to settle a trade. We just need a secure place where our Agents can meet, exchange verifiable facts, sign the deal and receive the output facts.

The End of the Platform

This shifts the power dynamic of the internet.

Currently, if you want to trade, you must go to a Platform (an Exchange, a Bank, a Marketplace). You are a user in their house.

In this new model, the “House” is temporary. You and your counterparties summon the infrastructure you need, use it, and discard it.

You are no longer a “User” logging into a portal. You are a Peer negotiating in a private room.

This leaves us with one final, critical question. We have the Identity (the Agent) and the Location (the Meeting Room). But what are we actually swapping to settle the deal? If money isn’t a token, what does it look like inside this room?

In the next chapter, we will look at Active Money—and why your bank account is about to wake up.

Chapter 3: Active Money

If there is one thing that defines the “Tokenization” mindset, it is the obsession with inventing new money. Stablecoins, crypto-tokens, central bank digital currencies (CBDCs)—everyone is trying to build a better digital coin.

But the problem with modern finance isn’t the money. The money is fine. It does not need to be fixed. It just needs to be made usable to settle digital contracts. It must be recognized as money in the digital rooms where all interaction is based on verifiable claims.

Most of the world runs on commercial bank money—the digital credits in your checking account. This money is regulated, insured, and accepted everywhere. The problem isn’t the asset itself; the problem is that it is Passive.

Your bank account is a dumb bucket. It sits there, inert, waiting for an instruction. To move money, you (or a payment processor) have to log in, send a command, and then wait. You have to wait for the bank to check the balance, wait for the clearinghouse to batch the file, and wait for the receiving bank to credit the other side.

The Internet Trust Layer (ITL) doesn’t try to replace your money with a new token that has to be reconciled with the existing system. It simply wakes your money up.

CoBDC: Commercial Bank Digital Currency (Done Right)

I call this concept CoBDC (Commercial Bank Digital Currency), but don’t let the acronym scare you. The little “o” is there for a reason. It’s not a new currency issued by the Central Bank. Neither is it a stablecoin. It definitely is not a token. It is simply Active Money that you already possess in your commercial bank account.

In the ITL, your bank operates a special piece of software called a Sub-Contract Agent (or “Integration Agent”). This agent acts as a secure bridge between the bank’s legacy database and the digital world of contracts.

When you want to buy something, your Person Agent doesn’t send a “token.” It pings your bank’s agent and says: “I need to prove I have $100 for this specific contract.”

The bank’s agent checks your balance, locks the funds, and then enters the Digital Meeting Room (the Context Agent) we discussed in the last chapter. It presents a cryptographically signed Verifiable Claim:

“Bank A certifies that this transaction is funded, should it finalise.”

This is subtle but revolutionary. The money hasn’t left the bank. It hasn’t been turned into a risky crypto-token that travels in a network of public transaction logs. It is still a commercial bank liability, private and protected by all existing laws. But it has become Active. It is now represented by an autonomous agent that can negotiate, prove, and settle instantly inside a digital contract.

The “Atomic” Settlement

This brings us to the killer feature of Active Money: The Contract IS the Settlement.

In the old world, the “Deal” (signing the contract) and the “Settlement” (moving the money) were two different events, separated by days of risk and reconciliation. This gap is why we have massive, expensive clearinghouses.

In the ITL, these two events are collapsed into one.

Inside the Digital Meeting Room, the logic is “Atomic.” This is a computer science term meaning “all or nothing.”

The Context Agent holds the Seller’s Title Deed (Claim) in one hand and the Buyer’s Money (Claim) in the other.

It verifies both.

It swaps them instantly.

It issues the final receipts, that bind the parties legally.

If anything fails—if the funds aren’t there, if the title is bad—the whole deal reverts. Nobody loses anything. But if it succeeds, it succeeds instantly and binds every party. The moment the contract is finalized, the settlement is done.

We just eliminated the need for a clearinghouse, not by building a faster pipe, but by building a smarter contract.

The “Airplane Mode” Test

There is one final test for any form of digital money: Does it work when the lights go out?

We have all had that moment of panic when the card terminal can’t connect, or your phone has no signal. In a fully digital world, if the internet goes down, do you starve?

Tokens claim to solve this, but usually require syncing with a blockchain eventually. Active Money solves it by mimicking physical cash.

Your Person Agent, or at least some critical part of it, especially the private key, lives in a secure enclave on your phone (a hardware chip). Your bank can issue a special “Offline Credential” to your phone—essentially loading $200 of digital cash into your secure chip.

Now, you are on a plane. You want to buy a coffee from a flight attendant who is also offline.

You tap phones. Your secure chip talks to their secure chip.

Your agent proves it has the funds.

It signs a transaction transferring $5, a typical price for a cup of lukewarm coffee in an airplane, to the attendant.

It updates its internal ledger (a “monotonic counter”) to ensure you can’t spend that same $5 again.

The transaction is final. You walk away with the coffee. When the attendant lands and reconnects to the internet, their agent uploads the signed proof to their bank, and the settlement is reconciled.

This is the holy grail: the speed of digital, the legality of banking, and the resilience of cash.

We don’t need to rebuild the financial system from scratch, let alone change its operating logic from contracts between accountable parties to barter between strangers. We don’t need to create new money issued by new parties who don’t have a proper framework for risk management. We just need to give our existing money a voice. We’re giving banking the generational upgrade it desperately needs.

In the final chapter, we will look at the biggest hurdle of all: The “Authorisation Crisis”—and why corporations are currently second-class citizens on the internet.

Chapter 4: The Authorization Crisis

If the “Wallet” is a poor metaphor for individuals, it is a catastrophic one for corporations.

In the previous article, we established that modern businesses need Organization Agents—autonomous servers that act as sovereign peers, rather than “Clients” logging into a portal. But when we apply this to finance, we run into the “Keys to the Castle” problem.

If an autonomous software agent holds the keys to the corporate bank account, who controls the agent?

In the current paradigm (the “Wallet Model”), we manage corporate authority by sharing secrets. If the CFO needs to make a transfer, they need the password to the banking portal. If the accounts payable team needs to pay invoices, they need the API keys or the shared login.

This is a security nightmare. It creates a brittle perimeter where “access” is binary: you either have the keys to the vault, or you don’t.

Moving from Access to Delegation

The Tokenization Trap isn’t just about the asset; it’s about the permission to move the asset. The Internet Trust Layer solves this not by sharing keys, but by Delegation.

In this model, the Organization Agent holds the “Root Identity” of the company. It never acts on a whim. It acts only when presented with a valid, cryptographically signed mandate from an authorized internal source.

It does not give the CFO the password to the bank. Instead, it issues a Verifiable Credential to the CFO’s personal User Agent.

This credential functions as a digital power of attorney. It might say:

“The bearer of this credential (CFO) is authorized by Acme Corp to sign transactions up to €10M.”

Simultaneously, it might issue a restricted credential to a summer intern:

“The bearer of this credential is authorized to order lunch up to €50.”

The End of the “Company Login”

When the CFO signs a deal, they do not “log in” as the company. They join the transaction context as a representative of the company and sign with their own private key, using their own agent. They simply attach the company’s “Authorization Credential” to the transaction.

The counterparty (or the bank) validates two things instantly:

Identity: Is this signature truly from the CFO?

Authority: Does this person hold a valid, unrevoked mandate from the Company to move this amount of money?

This is the holy grail of treasury management: Granular, Revocable Authority.

If the CFO quits, or the intern is fired for ordering vegan lunch only, the company does not need to change banking passwords or rotate API keys. The Organization Agent simply revokes that specific credential. The authority vanishes instantly. The ex-employee still has their agent, but it is now powerless to spend company funds.

Policy-as-Code

This logic extends beyond humans to machines. We can move from “manual approval” to Computational Trust in contexts where decision-making can be automated.

Imagine a supply chain scenario. A supplier submits an invoice. In the “Wallet” world, this sits in an inbox waiting for a manager to log in and approve it.

In the Agent world, the Organization Agent checks its internal Policy-as-Code.

Did the Warehouse Agent sign a proof that goods arrived? Yes.

Is the invoice amount within the pre-approved budget? Yes.

Is the supplier on the verified whitelist? Yes.

The Agent signs the payment immediately.

We are not just digitizing the payment; we are digitizing the Resolution. We are replacing the “Client” that waits for permission with a “Peer” that enforces policy.

This is the final piece of the puzzle. We have the Context (The Meeting Room), the Asset (Active Money), and the Authority (The Delegate).

The future of finance is not about building better tokens to put in our wallets. It is about building better relationships between our agents.

Conclusion: The End of the Interface

We are entering a strange new era of the internet. For decades, “Digital Transformation” meant building better user interfaces—slicker apps, prettier dashboards, faster portals. APIs everywhere.

The next era is about The End of the Interface.

The most efficient digital transaction is the one you never see. It is the hotel check-in that happens before you walk through the door. It is the invoice that settles itself the moment the cargo lands. It is the loan that approves itself the second the criteria are met.

This future cannot be built with Wallets, Tokens, or Client Apps accessing service APIs. These are all tools designed to help humans interact with machines.

The future belongs to Agents—tools designed to help machines interact with machines, on our behalf, under our strict control.

The Token is a dead end. The Wallet is a skeuomorph. The future is the Relationship.

The “wallet war” may keep on raging for a good while, because the main combatants are not running out of money any time soon, but with a good probability, its winner will not rule the world. The winner, if there is any, will have built a better front-end to an utterly outdated back-end. It is time to stop building digital casinos and start building a verifiable economy.